Considerations for Settling Transfer Pricing Disputes in Multinational Enterprise (MNE) Dealings

Introduction

Over 130 countries – including some that are reputed tax havens – have, in recent years, moved to align their tax policies.[1] Consequently, Multinational Enterprises (MNEs) will sustain a higher tax floor as countries adapt a global minimum corporate tax rate (GMT)[2], and bear more oversight as standardized transfer pricing methods are instituted.[3] The latter proposition should also achieve coherence in litigations between MNEs and regulatory bodies concerning matters of settling transfer pricing[4] disputes.

Background

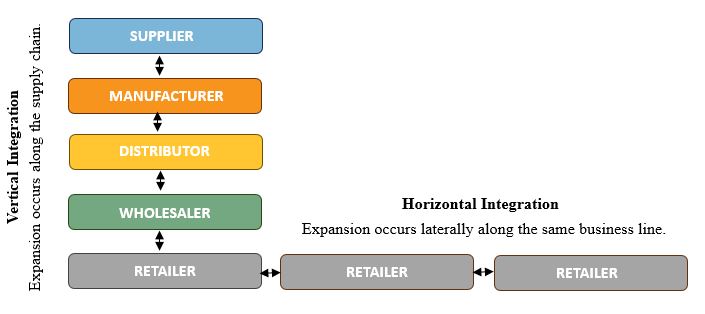

MNEs are those entities headquartered in one country – referred to as the home country – that engage in trade through extensions of their value chain in other countries – sometimes referred to as host countries. One rationale for companies to expand their operations internationally is a potential for increased revenues arising from competitive advantages gained by scaling operations, such as reduced costs of production, increased bargaining power, product diversification, and capturing and/or servicing new markets. As the graphic below illustrates, companies may integrate vertically (e.g., adding a retail function) or horizontally (e.g., adding to already existing retail functions) across borders. However, once a company expands its operations to other countries, it is also exposed to potential disputes, including disputes over transfer pricing.

Transfer pricing disputes may arise when prices charged by an entity to its overseas affiliate(s) are alleged to have been inconsistent with those charged to third parties for comparable transactions under comparable circumstances. As stated in Article 9 of the OECD Model Tax Convention, the “arm’s length principle” is an international standard enforceable when “conditions are made or imposed between the two enterprises in their commercial or financial relations which differ from those which would be made between independent enterprises, then any profits which would, but for those conditions, have accrued to one of the enterprises, but, by reason of those conditions, have not so accrued, may be included in the profits of that enterprise and taxed accordingly.”[5] Therefore, each party of an intercompany transaction should deal at arm’s length with the other. When affiliated parties are suspected of breaching the “arm’s length principle,” then a tax or regulatory authority may pursue legal or administrative actions to remedy the alleged mispricing.

The OECD Guidelines

Many countries have developed their own domestic standards and guidelines for assessing arm’s length pricing. However, the Organization for Economic Co-operation (OECD), which is an international organization comprising 38 member states that meet to “[establish] evidence-based international standards and [find] solutions to a range of social, economic and environmental challenges,”[6] has also established guidelines. The OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations (“OECD Guidelines”) provide frameworks that may be applied when evaluating the considerations received by affiliated entities.

Establishing Comparability Factors

In substantiating claims regarding potential breaches of the arm’s length principle, it is pivotal that like is compared with like, i.e., the transactions in question are comparable. The OECD Guidelines list five economically relevant characteristics[7] to help assess the degree of comparability:

- The contractual terms of the transaction,

- The functions performed by each of the parties to the transaction,

- The characteristics of property transferred or services provided,

- The economic circumstances of the parties and of the market in which the parties operate, and,

- The business strategies pursued by the parties.

Transfer Pricing Methodologies

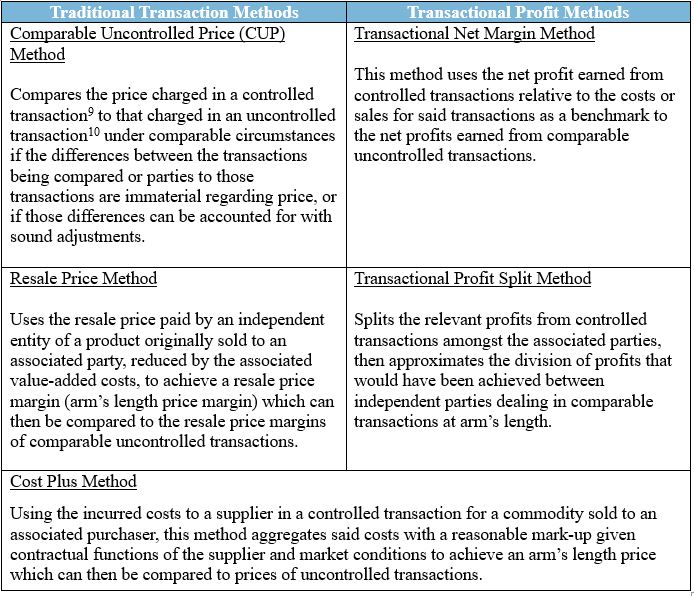

The OECD Guidelines also discuss methods for applying the arm's length principle, namely, traditional transaction methods and transaction profit methods. These are listed in the table below.[8] In addition, unspecified methods may be acceptable.

Application of Transfer Pricing Methodologies (TPM) in Litigation

The Coca-Cola Company & Subsidiaries v. Commissioner of Internal Revenue, 155 T.C. 145 (2020)

A November 2020 ruling by the United States Tax Court (“U.S. Tax Court”) in favor of the Internal Revenue Service (IRS) increased Coca-Cola’s U.S. based taxable income for FYs 2007-2009 by some USD $9 billion – less a concession of USD $1.8 billion – following disputes regarding Coca-Cola’s compensation from its Intellectual Property (IP) licensed to its affiliated foreign manufacturers (supply points) in Brazil. This judgement was handed down subsequent to the IRS’ disputed reallocation of income between Coca-Cola and its supply points based on a comparable profits method (CPM), which applied the ratio of operating profit to operating assets (ROA)[11] of independent bottlers as comparable parties for assessing the arm’s length considerations between Coca-Cola and its supply points. The CPM approach – in lieu of the profit split method – and ROA are appropriate estimators in this case given that neither the implications of the licensed intangibles (IP) were directly linked to any costs or inputs associated with production of the Coca-Cola products, nor did the supply points contribute significantly to Coca-Cola’s intangibles that were employed in their manufacturing process.

Since the U.S. Tax Court’s ruling in this litigation in 2020, Brazil has aligned its transfer pricing legislation with the OECD Guidelines, subsequently introducing “new concepts into Brazilian law that are relevant to determining the arm’s length principle, such as the delineation of the transaction, and the functional and comparability analysis.”[12] Brazil’s adaptation of the OECD Guidelines into its legal framework signals the legitimacy and applicability of the OECD’s standardized set of methods in settling transfer pricing disputes in MNE dealings.

CITATIONS

[4] “Transfer pricing refers to prices in transactions between two companies in the same corporate group. Tax authorities require those prices to be similar to those found in a transaction between arm’s length firms to keep companies from artificially lowering their tax bills.” Source: https://news.bloombergtax.com/daily-tax-report-international/major-firms-seek-to-shift-transfer-pricing-law-landscape-in-2024

[5] OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2022, Page 19

[6] https://www.oecd.org/about/

[7] OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2022, Chapter 1, ¶ D.1.36.

[8] OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2022, Chapter 2

[9] Controlled transactions refer to those transactions between affiliated entities.

[10] Uncontrolled transactions refer to those transactions between unaffiliated entities.

[11] ROA = Operating Income / Total Assets

Experts

Marlon BrooksConsultant

Marlon BrooksConsultant